“New Tax Reform: What it Means for the Real Estate Market in Queens NY”, Provided by the Queens Home Team at Keller Williams Realty Landmark II. Need help, feel free to Contact Us anytime.

Congress has just passed the most sweeping tax code overhaul in decades and making sense of al the changes can be somewhat complex. Now, as local real estate agents in Queens, it is not only important for us to understand the new tax reform specifics, but also how they will impact the local Queens real estate market. Many of these new provisions will kick in on January 1, 2018 and several will expire after 2025. With that said, below is a summary of of the recently passed changes as well our best attempt to anticipate how these changes will affect our local real estate market.

Introduction

Based on most of the changes passed, it seems that the overall structure of the new bill pretty much diminishes the tax benefits of homeownership. As a result, this bill will likely cause adverse impacts in some markets like Queens because we have high value properties, state taxes, and local taxes. (katieaustin.tv) The good news is that our property taxes are not as high as those in Long Island or New Jersey so in that respect, we are fortunate. Ultimately, it looks like the final legislation will benefit many homeowners, homebuyers, and real estate investors, but it will also hurt some people as well.

I think the new changes will definitely have an affect on our local market in 2018, although I don’t think it will be as bad as what we we may see in Long Island and New Jersey. People who own homes valued at or above $1M may see the biggest impact on their home’s value. Demand may dip overall because many of the new tax changes eliminate the tax benefits of homeownership. For tax purposes renting and owning are pretty much the same. As a result, we may see a drop off in demand from homebuyers who incentivized by tax benefits of homeownership.

As a result of the changes made throughout the legislative process, NAR (National Association of Realtors) is now projecting slower growth in national home prices of 1-3% and in high cost & higher tax ares, the NAR is predicting price declines mainly because of the legislation’s new restrictions on mortgage interest and state and local taxes.

The information provided is for illustrative purposes and based on a our understanding of the final legislation as of December 20, 2017. If you have questions, you should consult a tax professional about your own personal situation. If you need a recommendation, we have some great CPAs that we can connect you with.

All individual provisions are generally effective after December 31, 2017 for the 2018 tax filing year and expire on December 31, 2025 unless otherwise noted. The provisions do not affect tax filings for 2017 unless noted.

Major Provisions affecting Current and Prospective Queens Homeowners

Tax Rate Reductions

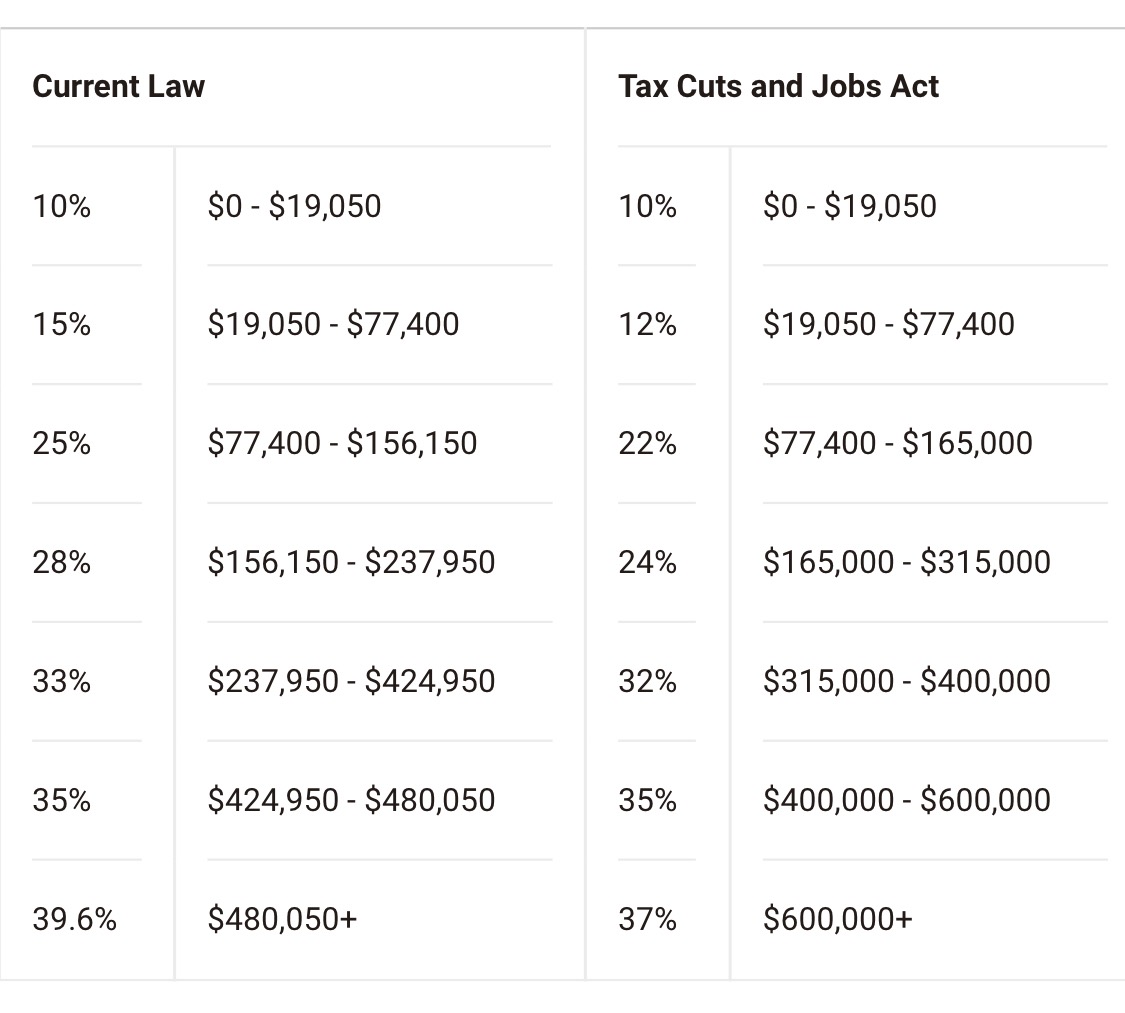

The new law provides generally lower tax rates for all individual tax filers. While this does not mean that every American will pay lower taxes under these changes, many will. The tax rate schedule retains seven brackets with slightly lower marginal rates of 10%, 12%, 22%, 24%, 32%, 35%, and 37%.

The final bill retains the current-law maximum rates on net capital gains (generally, 15% maximum rate but 20% for those in the highest tax bracket).

Tax Brackets for Ordinary Income Under Current Law and the Tax Cuts and Jobs Act (2018 Tax Year) – Single Filer

Tax Brackets for Ordinary Income Under Current Law and the Tax Cuts and Jobs Act (2018 Tax Year) – Married Filing Jointly

Exclusion of Gain on Sale of a Principal Residence

The final bill retains current law which means that a homeowner must live in their property for 2 of the last 5 years in order to qualify for the exclusion. The Senate-passed bill would have changed the amount of time a homeowner must live in their home to qualify for the capital gains exclusion from 2 out of the past 5 years to 5 out of the past 8 years. The House bill would have made this same change as well as phased out the exclusion for taxpayers with incomes above $250,000 single/$500,000 married. This is good news for all Queens homeowners.

Mortgage Interest Deduction

The final bill reduces the limit on deductible mortgage debt to $750,000 for new loans taken out after 12/14/17. Current loans of up to $1 million are grandfathered and are not subject to the new $750,000 cap. This new provision will definitely affect Queens homeowners because many of our single and multi-family homes sell close to and over a million.

Homeowners may refinance mortgage debts existing on 12/14/17 up to $1 million and still deduct the interest, so long as the new loan does not exceed the amount of the mortgage being refinanced.

The final bill repeals the deduction for interest paid on home equity debt through 12/31/25. Interest is still deductible on home equity loans if the proceeds are used to substantially improve the residence.

Interest remains deductible on second homes, but subject to the $1 million / $750,000 limits.

The House-passed bill would have capped the mortgage interest limit at $500,000 and eliminated the deduction for second homes.

State and Local Tax Deduction (SALT)

The final bill allows an itemized deduction of up to $10,000 for the total of state and local property taxes and income or sales taxes. This $10,000 limit applies for both single and married filers and is not indexed for inflation. The final bill also specifically precludes the deduction of 2018 state and local income taxes prepaid in 2017.

When House and Senate bills were first introduced, the deduction for state and local taxes would have been completely eliminated. The House and Senate passed bills would have allowed property taxes to be deducted up to $10,000. The final bill, while less beneficial than current law, represents a significant improvement over the original proposals.

Standard Deduction

The final bill provides a standard deduction of $12,000 for single individuals and $24,000 for joint returns. By doubling the standard deduction, Congress has greatly reduced the value of the mortgage interest and property tax deductions as tax incentives for homeownership. Congressional estimates indicate that only 5-8% of filers will now be eligible to claim these deductions by itemizing, meaning there will be no tax differential between renting and owning for more than 90% of taxpayers.

Repeal of Personal Exemption and Dependent Deductions

Under the prior law, tax filers could deduct $4,150 for the filer and his or her spouse, if any, and for each dependent. These exemptions have been repealed in the new law. This change alone greatly mitigates (and in some cases entirely eliminates) the positive aspects of the higher standard deduction.

When combined with the increased standard deduction and increased child tax credit, lower- and middle-income households should see a net benefit despite the elimination of these deductions. However, higher-income taxpayers could see an increased tax bill from this proposal if they have large families and don’t qualify for the child tax credit, because of the income phase-outs within the tax bill.

Child Tax Credit

The final bill increases the child tax credit to $2,000 from $1,000 and keeps the age limit at 16 and younger. The income phase-out to claim the child credit was increased significantly from ($55,000 single/$110,000 married) under current law to $500,000 for all filers in the final bill.

Tax credits are generally better than tax deductions, because credits reduce your taxes dollar-for-dollar, while deductions only lower your taxable income. This change would benefit low- and middle-income households with children.

Student Loan Interest Deduction

The final bill retains current law, allowing deductibility of student loan debt up to $2,500, subject to income phase-outs. The House bill would have eliminated the deduction for interest on student loans.

Moving Expenses

The final bill repeals moving expense deduction and exclusion, except for members of the Armed Forces. The House-introduced bill would have eliminated the moving expense deduction for all filers, including military.

Like-Kind Exchanges or 1031 Exhanges

The final bill retains the current Section 1031 Like Kind Exchange rules for real property. It repeals the use of Section 1031 for personal property, such as art work, auto fleets, heavy equipment, etc.

The exclusion of real estate from the repeal of 1031 like-kind exchanges is a major victory for real estate stakeholders, who had fought hard to preserve the provision for several years, and against long odds.

Summary

In general, if you don’t normally itemize your deductions, these changes won’t be an issue and the increased standard deduction should end up benefiting you. However, if you’re in a high income household in a high tax state with a mortgage and high property taxes, these changes could end up increasing your tax liability. As local Realtors, we know that there are several high income households in Queens, and being that we live in NYC, we have city as well as state taxes. Fortunately our property taxes are not that high, but it looks like high income homeowner households in Queens will likely end up losing from this deal.

The new tax reform seems to diminish many of the benefits of homeownership and tax benefits of homeownership have always been a big incentive for people to strive towards owning a home. Based on what we’ve learned about the new tax bill, it seems to essentially make renting the same as owning and as a result, we may see an affect on buyer demand. Many of our Associates are predicting a shift in the market as a result of this new tax bill. 2017 already began to feel much softer than the last two years and this new reform may be what leads to a more pronounced shift in the market. We will watch sales and home prices closely to keep you informed as things change. In the meantime, if you have any questions or need any advice, feel free to contact us anytime.