Data Source: Reference Guide to 1031 Exchanges, Courtesy of Ryan Vassar, Esq. Vice President at IPX 1031

What is a 1031 Exchange?

“No gain or loss shall be recognized on the exchange of real property held for productive use in a trade or business or for investment if such real property is exchanged solely for real property of like-kind which is to be held either for productive use in a trade or business or for investment.”

Translation: You don’t have to pay taxes on the profit (or claim a loss) when you swap one investment or business property for another similar property, as long as:

- The property you’re giving up was used for business or investment (not your primary home), and

- The property you receive is also real estate, and

- You plan to use the new property for business or investment purposes too.

In short:

👉 If you trade one investment property for another investment property, the IRS lets you delay paying taxes on the gain.

Determining Your Capital Gain

Original Purchase Price + Non-expensed Improvements – Depreciation Taken = Adjusted Basis

Example:

Purchased for $300,000 (Initial Cost Basis)

- $50,000 in Improvements

- $100,000 in Depreciation

- Adjusted Cost Basis = $250,000 ($300,000 – $50,000 + $100,000)

So if you were to sell for $650,000, your capital gain would be: $400,000 ($650,000 – $300,000 – $50,000 + $100,000)

What Taxes Are You Deferring?

Current Tax Rates

FEDERAL CAPITAL GAINS TAX – 15 – 20% (20% for single filers with income exceeding $533,400.00 and married filers with income exceeding $600,050.00)

3.8% HEALTHCARE TAX (still in under “Tax Cuts and Jobs Act”)

Surtax on certain “net investment income” (dividends, cap gains, partnership income, retirement income)

Imposed on the amount in excess of – Single income over $200,000, Married over $250,000

Depreciation Recapture (25%)

State Taxes (10.9% in New York)

RUN THE NUMBERS

1031 permits deferral of:

Capital Gains Taxes (15-20% Fed, 10.9% State)

Depreciation Recapture (25%)

Net Investment Income Tax (NIIT) (3.8%)

Application of Tax Rates

EXAMPLE:

Example: Selling $1,000,000 property that has no debt and has been fully depreciated. Using an assumption of a 35% of total tax burden.

This is an example of just one transaction. Multiply this result with all of the buying and selling you will do over the course of your life and you can imagine how much larger your net worth will be by the time you retire.

WHY 1031?

Motives for a 1031 can include…

Cashflow – Sell vacant land; acquire improved property to generate cash flow.

Depreciation – Exchange from fully depreciated property to a higher value property – the additional value can be depreciated.

Appreciation – Dispose of property in a slow market area and acquire property in a hot market area.

Conversion – Acquire separate properties so that co-owners can separate interests.

Joint Ownership Problems – Acquire property suitable for future conversion to primary residence or vacation home.

Reduce Management Burdens – Acquire management-free property.

Estate Planning – Dispose of one property and acquire several properties (example: distribute one replacement property to each family member).

Use in Profession – For example, a doctor sells a rental house and acquires a medical building to support the practice.

WHAT IS LIKE-KIND PROPERTY?

In an IRC §1031 real property exchange, as a general principle you can exchange real property for any other real property in the United States, if said property is held for productive use in a trade or business or for investment purposes.

1031 Property

RETAIL

APARTMENTS

SINGLE FAMILY

RAW LAND

INDUSTRIAL PROPERTY

COMMERCIAL

% INTEREST AS A TIC

WHAT IS NOT LIKE-KIND PROPERTY?

Not 1031 Property

PARTNERSHIP INTERESTS

STOCKS, BONDS, NOTES

PRIMARY RESIDENCE/VACATION HOMES

OTHER SECURITIES – OR EVIDENCE OF INDEBTEDNESS

CERTIFICATE OF TRUST – OR BENEFICIAL INTERESTS

STOCK IN TRADE – OR OTHER PROPERTY HELD PRIMARILY FOR SALE (INVENTORY)

SAME TAXPAYER REQUIREMENT

With a few exceptions in an exchange, title to the Replacement property is usually held in the same manner as title was held on the Relinquished property.

The same taxpayer that sells the Relinquished property must acquire the Replacement property.

BASIC RULES OF §1031 TIME FRAMES

What is day zero in an exchange? ➔ Transfer of Benefits & Burdens of Ownership

When do you need to open your exchange? ➔ Before you close on the Relinquished Property

The Exchanger must identify the property to be purchased within 45 days following the transfer of the Relinquished Property.

The Exchanger must close on the Replacement Property within 180 days.

Only One Exception – Federal Disaster Exemption

THREE RULES OF IDENTIFICATION

THREE PROPERTY RULE – The Exchanger may identify up to three properties of any value.

200% RULE – The Exchanger may identify more than three properties if the total fair market value of what is identified does not exceed 200% of the fair market value of the relinquished property(ies).

95% EXCEPTION – If the Exchanger identifies properties in excess of both Rule 1 and Rule 2, then the Exchanger must acquire at least 95% of the value of all properties identified.

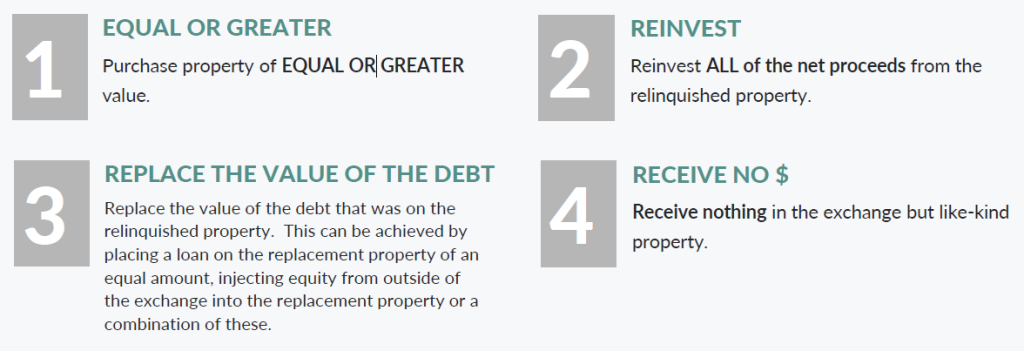

BASIC 1031 RULES

In order to obtain a deferral of the entire capital gain tax the Exchanger must:

To the extent the Exchanger fails to observe these rules they will be subject to capital gain tax on what is not reinvested.

QUALIFIED INTERMEDIARY, WHAT IS THEIR JOB?

Acts as a Principal – Exchangers must assign to a Qualified Intermediary: their interest as seller of the relinquished property, and their interest as buyer of the replacement property.

Holds Exchange Proceeds – If the Exchanger actually or constructively receives any of the proceeds from the sale of the relinquished property, those proceeds will be taxable.

Prepares Legal Documentation – Several legal documents are necessary in order to properly complete an exchange. The Qualified Intermediary will prepare an Exchange Agreement, two Assignment Agreements, and Exchange closing instructions.

Provides Quality Service – Although the process is relatively simple, the rules are complicated and filled with potential pitfalls.

As you can imagine there are many more variables involved with a 1031 exchange. This is a basic breakdown designed to give you an idea of the process, requirements, qualifications, etc. If you have any questions, feel free to Contact Us. And if you’re thinking of doing a 1031 exchange and need a Qualified Intermediary, feel free to contact Ryan Vassar, Esq. at IPX 1031.