Information provided by Claddagh Capital LLC

What is a Cap Rate and why its important?

A Capitalization Rate or cap rate is a metric used in commercial real estate to assess the return and risk of a property, purchased on an all-cash basis or unleveled (no mortgage).

The cap rate is used on an unleveled basis as it allows an investor to evaluate similar properties based on their Net Operating Income (NOI) regardless of how the property is financed.

It is essential to be aware of the current market conditions and cap rate for the asset class in question. Cap rates are market-specific and in constant flux. In addition, cap rates are influenced by multiple market forces, including investor demand, availability of capital, local economic conditions, property inventory, and growth prospects, to name a few.

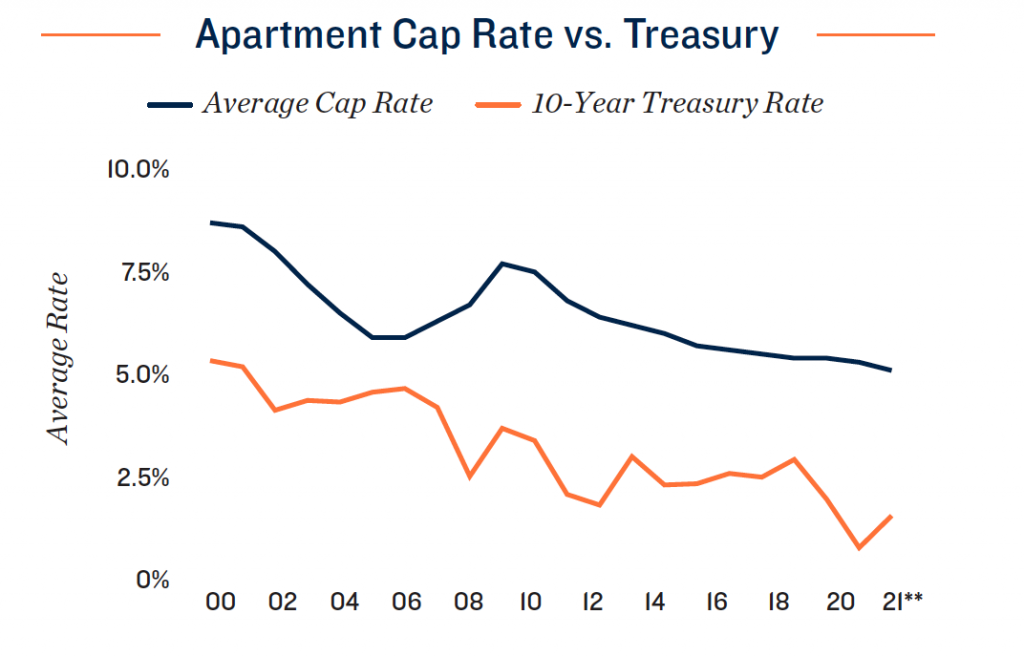

In general, higher cap rates translate to higher risk in the investment, while lower cap rates indicate less risk and a more stabilized asset. Many investors look at the Cap Rate Spread or diffrence over what they could earn risk-free on a 10 year Treasury, and evaluate if the investment meets their return and risk tolerance expectations for the capital deployed.

| Cap Rate = | Net Operating Income Market Value |

If you know the current cap rate in a market for the asset class, you can determine the property value or purchase price based on the NOI and quickly compare it to similar assets.

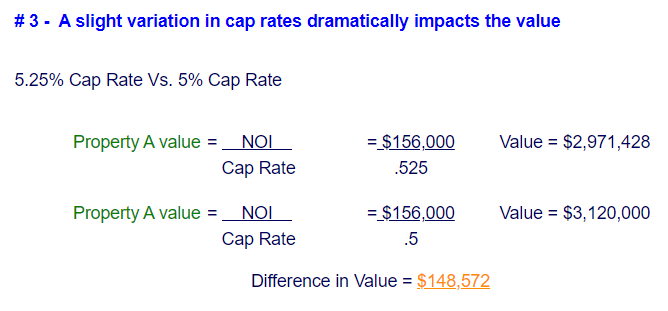

It is important to note that just a $13,000 difference in NOI between property A and B significantly impacts value by almost $250,000

Accurate cap rate information is vital, so you don’t overpay if you are buying a property and don’t under price your property if you are selling.

Limitations of Cap Rates

As you see above in item #2, a $13,000 difference in NOI between two assets can materially impact the value. If the purchaser is considering a “Value Add” property, the market cap rate is not always effective in determining what the property is worth. Why is that? In many cases, a “value add” buyer may be willing to pay more for the property (a lower cap rate) than the current NOI and stabilized market cap would justify. This is because they are forecasting they can generate a higher NOI than a stabilized property with limited opportunity for NOI growth.

A value-add buyer can use the current market cap rate to estimate what future cap rate to apply to their projected NOI at the time of disposition. However, it would be prudent to use a higher exit cap rate than the current market when evaluating the deal to account for unknown market forces between acquisition and disposition. A general rule of thumb is to increase the exit cap rate by ten basis points (1/10 of 1%) for each year the property is held.

To learn more about investing in multifamily apartments and whether you may be an accredited or sophisticated investor contact www.Claddagh-Capital.com